Thinking about refinancing your loan but worried about the costs? You’re not alone.

Refinancing can save you money, but only if you understand exactly what it will cost you upfront. That’s where a Loan Refinance Cost Calculator becomes your best friend. It helps you see the full picture—how much you’ll pay now, how much you’ll save later, and when your savings will actually outweigh your expenses.

If you want to make smart financial decisions and avoid surprises, keep reading. This guide will show you how to use a refinance cost calculator to take control of your loan and your future.

Refinance Costs To Expect

Recording fees and taxes are charged by the government to record your new loan. These fees vary by state and county. Loan origination fees are paid to the lender for processing the loan. They usually cost about 0.5% to 1% of the loan amount.

Appraisal and inspection charges pay for checking your home’s value and condition. These reports help the lender decide if the loan is safe. Title search and insurance protect you from legal problems with the property title. This ensures no one else owns your home.

Prepayment penalties are fees some lenders charge if you pay off your old loan early. Not all loans have this penalty. Always check your loan terms to avoid surprises.

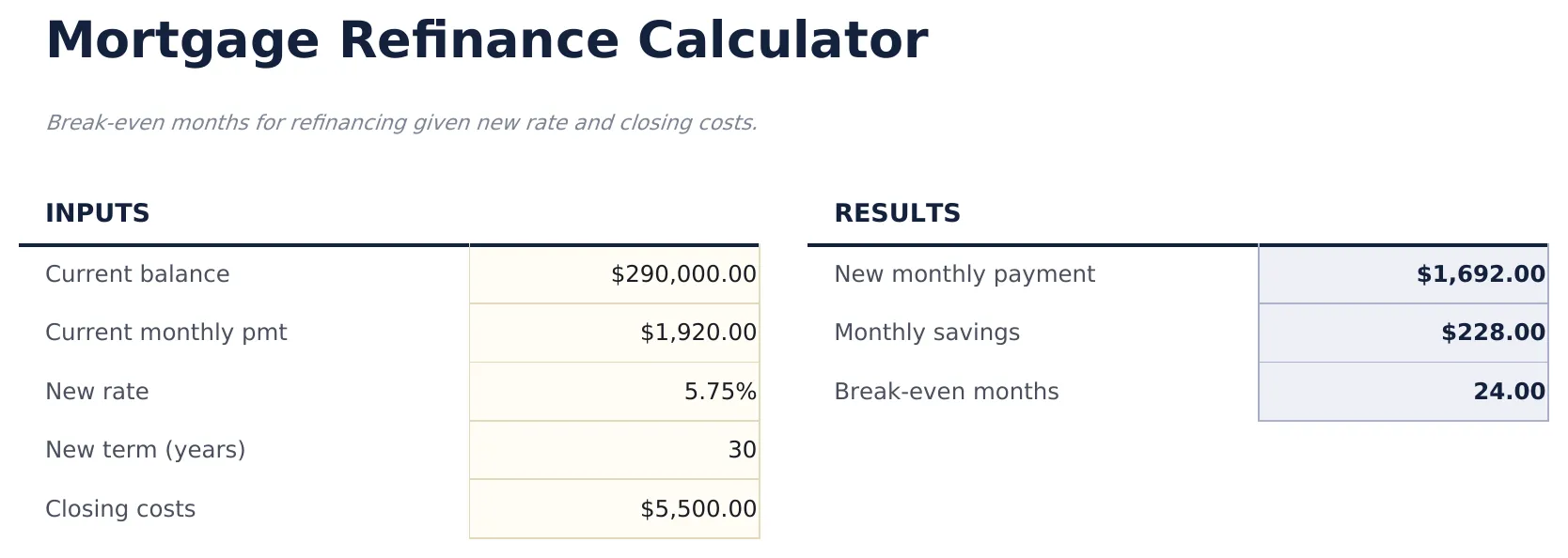

How To Use A Refinance Calculator

Start by entering your current loan amount and interest rate. Add the remaining loan term to get accurate results.

Next, input the new loan’s interest rate and term length. This helps estimate your new monthly payments and total interest.

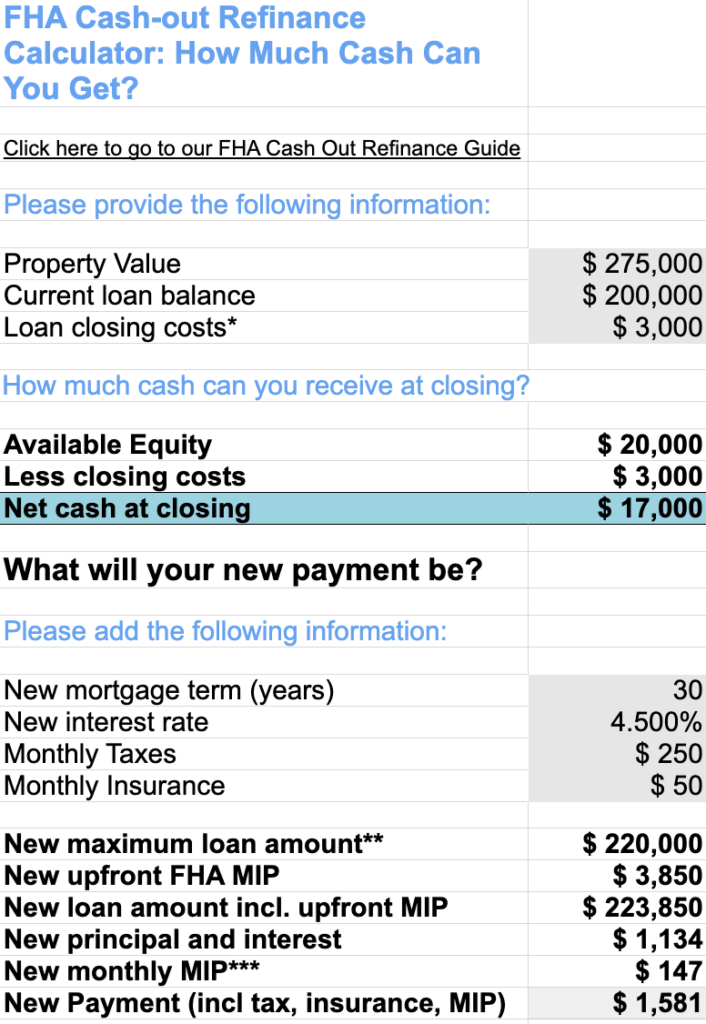

Include closing costs like fees for appraisal, title, and lender charges. These add to the refinance expense.

Adjust for loan points if you pay upfront fees to lower your new interest rate. This affects overall savings.

Compare your current monthly payment with the new one. Check how much you save each month and how long until you break even.

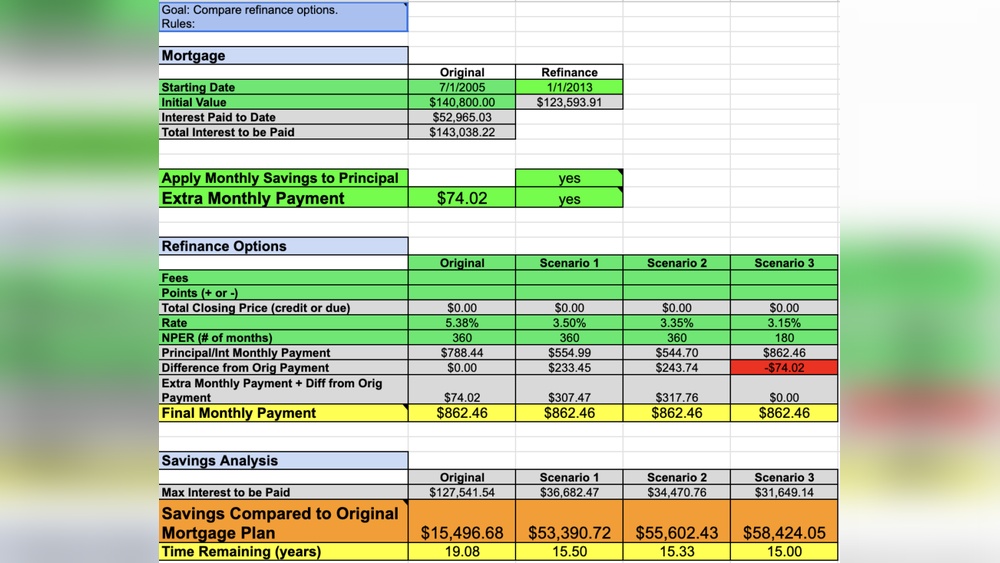

Calculating Your Break-even Point

Use the formula to find your break-even months:

Break-Even Months = Total Closing Costs ÷ Monthly Savings.

This number shows how many months it takes to recover refinancing costs. If you plan to stay longer than this, refinancing may save money.

Monthly savings come from lower payments after refinancing. Bigger savings mean a shorter break-even time.

Compare your break-even months to how long you will keep the loan. If break-even is short, refinancing can be worth it.

Benefits Of Refinancing With Smart Estimates

Maximizing monthly savings helps lower your regular payments. A refinance calculator shows how much you save each month. It compares your current loan with new options. This helps you pick the best plan for your budget.

Reducing interest over time means paying less total money to the lender. By refinancing to a lower rate, interest costs drop. Even small rate changes add up to big savings over years.

Shortening loan term options lets you pay off debt faster. A shorter loan means fewer interest payments. Your monthly payment might be a bit higher, but you save money overall.

Avoiding unnecessary costs keeps refinancing affordable. Smart calculators include fees like closing costs and taxes. They show if refinancing really saves money after all expenses.

Common Mistakes To Avoid

Ignoring hidden fees can cause surprises in refinance costs. These include recording fees, taxes, and lender points. Many borrowers overlook these fees, which add up quickly.

Overlooking break-even analysis means not knowing when savings start. Calculate break-even by dividing total closing costs by monthly savings. This helps decide if refinancing is worth it.

Failing to update loan information leads to wrong calculations. Always enter current loan balance, interest rate, and loan term for accurate results. Outdated info gives misleading outcomes.

Neglecting credit score impact risks higher costs. A low credit score may raise your interest rate. Check your score before refinancing to secure better terms.

Top Refinance Calculators Online

The Bankrate Refinance Calculator helps estimate your expenses, monthly savings, and break-even time. It’s easy to use and provides clear numbers.

Calculator.net Tool offers a visual comparison between your current loan and new loan options. This helps you see potential savings quickly.

The U.S. Bank Mortgage Calculator is useful for checking different refinance scenarios. You can adjust rates and terms to find the best fit.

Fannie Mae Refinance Calculator is designed for those considering government-backed loans. It shows how refinancing affects your payments and costs.

Tips For Lowering Refinance Costs

Negotiating lender fees can save you hundreds of dollars. Ask if some fees are flexible or can be waived. Some lenders may reduce or remove origination, processing, or underwriting fees to win your business.

Choosing no-closing-cost loans means higher interest rates but no upfront payments. This option spreads the refinance costs into your monthly payments. It works well if you plan to sell or refinance again soon.

Timing your refinance strategically helps lower costs. Interest rates and fees change often. Watch the market and refinance when rates are low. Also, refinancing early in the loan term often saves more money.

Improving your credit score before refinancing can reduce your interest rate. Pay down debts and fix errors on your credit report. A better score means better loan offers and lower fees.

Frequently Asked Questions

What Is The Typical Cost Of Refinancing A Loan?

The typical cost of refinancing a loan ranges from 2% to 5% of the loan amount. Fees include appraisal, origination, and closing costs. Use a loan refinance cost calculator to estimate your specific expenses and potential savings.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your total refinancing costs should not exceed 2% of your loan amount. This helps ensure savings outweigh costs.

How Much Does It Cost To Refinance A $300,000 Mortgage?

Refinancing a $300,000 mortgage typically costs between $3,000 and $6,000 in closing fees. This includes appraisal, origination, and title fees. Use a refinance cost calculator to estimate exact expenses and calculate your break-even point for savings.

How Much Does It Cost To Refinance A $400,000 Home?

Refinancing a $400,000 home typically costs 2% to 5% of the loan amount. This equals $8,000 to $20,000 in fees. Common fees include appraisal, title search, and lender charges. Use a refinance cost calculator to estimate exact expenses and potential savings.

Conclusion

Using a loan refinance cost calculator helps you make smart choices. It shows your fees and potential savings clearly. You can find your break-even point quickly with this tool. Knowing your costs upfront avoids surprises later on. Refinancing might lower your monthly payments and save money over time.

Take your time to compare offers before deciding. This simple step can lead to better financial health. Use the calculator often to keep track of your options. Stay informed and in control of your loan journey.