Are you wondering if now is the right time to refinance your home mortgage? Your mortgage refinance rate can make a big difference in your monthly payments and overall savings.

Knowing today’s rates helps you decide whether refinancing will lower your costs or improve your loan terms. You’ll discover how current home mortgage refinance rates work, what factors affect them, and how you can find the best deal for your situation.

Keep reading to take control of your mortgage and unlock potential savings that could put more money back in your pocket.

Current Refinance Rates

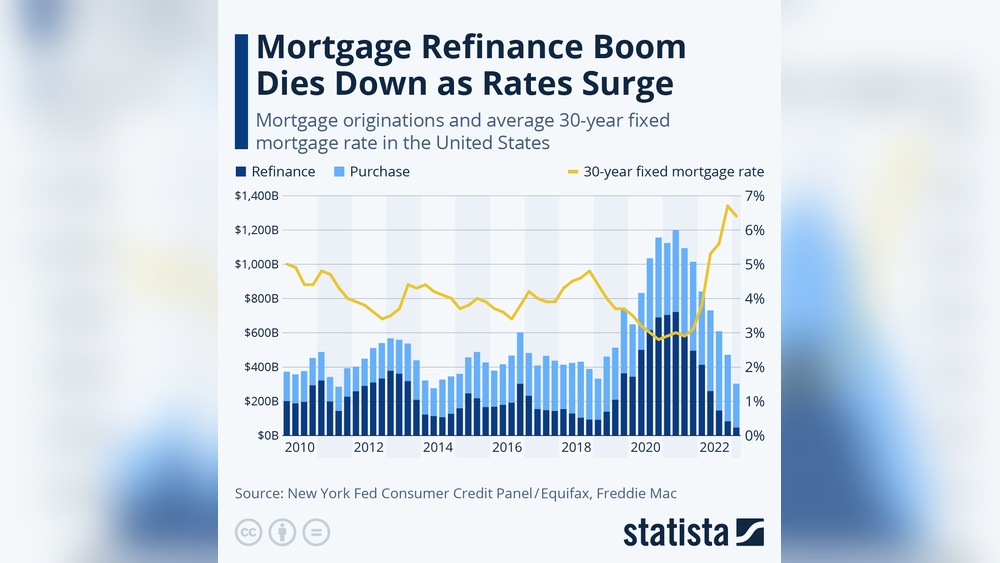

The national average refinance rate for a 30-year fixed mortgage is around 6.5%. Rates can be lower for 15-year loans, usually near 5.9%. In Austin, Texas, rates often align closely with the national average but may vary slightly due to local market conditions.

Several key factors influence refinance rates. These include:

- Credit score: Higher scores get better rates.

- Loan amount: Larger loans might have different rates.

- Loan type: Fixed vs. adjustable rates affect costs.

- Market conditions: Economic trends impact rates daily.

- Property location: Local real estate markets can cause rate changes.

Checking rates often helps find the best deal. Small differences in rates change monthly payments significantly.

Benefits Of Refinancing

Lower monthly payments help reduce your financial stress. Refinancing can lower your interest rate. This means smaller payments each month. You keep more money in your pocket. Easy to manage your budget this way.

Shortening loan term means paying off your home faster. You pay less interest over time. This saves thousands of dollars. Monthly payments might be higher, but total cost is less. Good for those who want to own home sooner.

Accessing home equity allows you to use your home’s value. You can get cash for big expenses. Examples: home repairs, education, or debt payoff. It can be a cheaper option than other loans. Just borrow against your house’s value.

Types Of Refinance Loans

Rate-and-Term Refinance helps change the loan’s interest rate or term. This can lower monthly payments or shorten the loan period. No extra cash is taken out with this type.

Cash-Out Refinance lets homeowners borrow more than they owe. The difference is given as cash. This cash can be used for home repairs, debts, or other needs.

Streamline Refinance is a faster process with less paperwork. It is for loans backed by government programs like FHA or VA. It usually has lower costs and easier approval.

:max_bytes(150000):strip_icc()/2-22Line-f1b1b2765f7243b896e202d28545054c.png)

How To Compare Refinance Deals

Interest rates show the yearly cost to borrow money, but APR includes fees too. APR gives a clearer picture of the total loan cost. Lower interest rates might seem good, but a higher APR means you pay more overall.

Closing costs and fees can add thousands to your loan. These include appraisal fees, title insurance, and lender charges. Always ask for a full list of these costs before agreeing to a deal.

Loan terms and conditions affect your monthly payments and total cost. Check how long the loan lasts and if you can pay early without penalties. Some loans have fixed rates, others change over time. Choose what fits your budget best.

Steps To Refinance Your Mortgage

Check Your Credit Score: Your credit score affects the refinance rate you get. A higher score means better rates. Get your score from free online services to see where you stand.

Gather Financial Documents: Collect recent pay stubs, tax returns, and bank statements. Lenders need these to verify your income and financial health.

Shop Around for Lenders: Compare offers from several lenders. Look at interest rates, fees, and terms. This helps you find the best deal for your needs.

Submit Application and Appraisal: Apply with your chosen lender. An appraiser will check your home’s value. This step is important for the lender to approve your refinance.

Common Refinancing Mistakes

Ignoring closing costs can make refinancing more expensive. Many people forget to add these fees when calculating savings. Closing costs include appraisal fees, loan origination fees, and title insurance. These costs can add up to thousands of dollars.

Refinancing too early may not be a smart choice. If you refinance soon after getting your original loan, you might pay fees without saving much. Usually, waiting at least 12 to 24 months helps you gain real benefits.

Choosing the wrong loan type can cause problems too. Fixed-rate loans offer steady payments, while adjustable-rate loans can change over time. Picking a loan that does not fit your needs can lead to higher costs or risks later.

Tools To Calculate Savings

Mortgage refinance calculators help estimate your new monthly payments. They show how much you can save by refinancing at a lower rate. Enter your loan details and new interest rate to get results fast.

Home value estimators give a quick estimate of your property’s current worth. This value helps decide if refinancing is a smart choice. It factors in local market trends and recent sales.

Break-even analysis shows how long it takes to recover refinance costs. It compares the upfront fees to monthly savings. Use this tool to know if refinancing saves money over time.

Refinancing Trends And Tips

Timing plays a big role in getting the best refinance rates. Rates may go up or down each day. Watching the market closely helps you choose the right moment to refinance.

Improving your credit score can lower your interest rate. Paying bills on time and reducing debt are simple ways to raise your score. A higher score means better loan offers.

Locking in a rate protects you from future increases. You can lock rates for a set time before closing the loan. This helps you avoid surprises if rates climb.

Frequently Asked Questions

What Is Today’s Interest Rate On A Refinance?

Today’s refinance interest rates vary by lender and credit profile but generally range between 6% and 7%. Check multiple sources for current rates.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new interest rate should be at least 2% lower than your current rate to save money. This helps ensure refinancing is financially beneficial by reducing monthly payments and overall interest costs.

How Much Is A $400,000 Mortgage Payment For 30 Years?

A $400,000 mortgage over 30 years typically costs about $2,100 per month at a 6% interest rate. Exact payments vary by rate. Use a mortgage calculator for precise figures based on current rates and loan terms.

Can A 70 Year Old Woman Get A 30-year Mortgage?

A 70-year-old woman can get a 30-year mortgage, but lenders consider income, credit, and ability to repay.

Conclusion

Refinancing your home mortgage can save you money over time. Rates change often, so check them regularly. Choose a rate that fits your budget and goals. Small savings add up to big benefits in the long run. Take your time to compare offers carefully.

Smart choices today can ease your financial future.